Section 1

Why Organizational Structure Matters in a Financial Model

A financial model does not exist independently of the institution it represents. It mirrors how the organization is governed, reported, and overseen.

Departments roll into divisions. Divisions roll into campuses or service areas. Funds roll into broader reporting frameworks. All of these relationships determine how financial activity is summarized and interpreted.

Organizational structure in a model serves as the bridge between operational detail and executive oversight.

Leaders rarely evaluate performance at the line-item level. They rely on summaries that reflect the institution’s hierarchy. If that hierarchy is inconsistently defined inside the model, even accurate calculations can produce confusing outputs.

Structure determines meaning.

When the model’s architecture mirrors organizational reality, users can trace results from institutional totals down to operational drivers. Without that clarity, reports require explanation rather than provide it.

Section 2

Organizational Structure in User-Managed Models

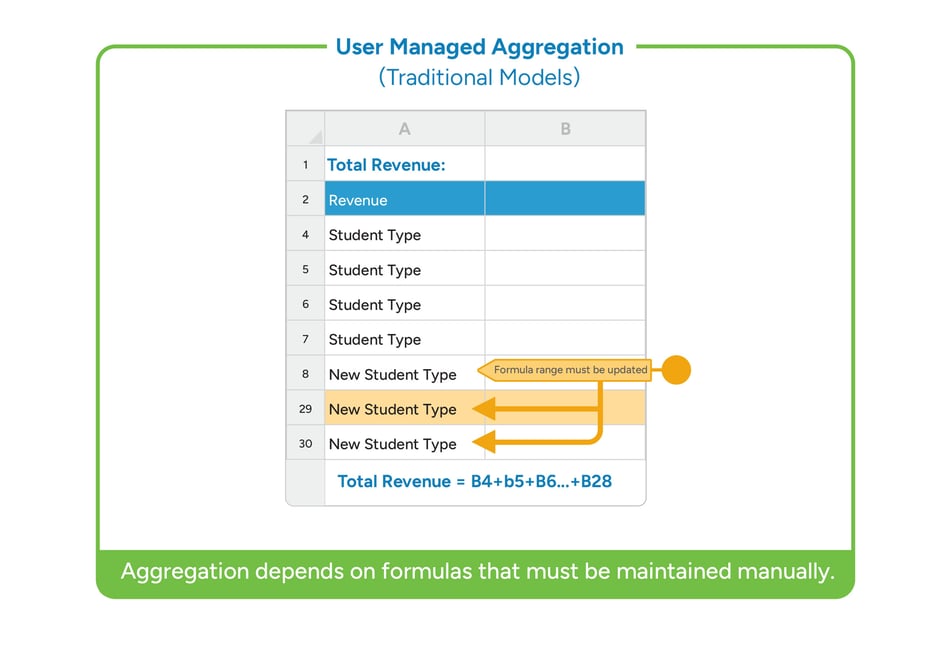

In traditional models, organizational structure typically begins as a blank slate. The modeler defines the reporting hierarchy, determines how financial elements roll up, establishes naming conventions, creates aggregation logic, and maintains consistency across outputs. This flexibility can feel empowering at first. The structure can be customized to meet immediate reporting needs or reflect a specific organizational preference. However, there are no embedded structural rules to guide or enforce consistency. Hierarchy and aggregation logic are defined manually and must be remembered, documented, and maintained by the user.

Over time, structure often evolves in response to short-term demands rather than long-term architectural planning. A new board report may require a modified roll-up. A reorganization may introduce additional layers. A new fund or regulatory requirement may add another reporting dimension. A one-time analytical view may create an exception to the existing hierarchy. Each adjustment adds complexity, and because user-managed models do not enforce structural governance, the model’s architecture can gradually become inconsistent across worksheets, dependent on institutional memory, vulnerable to misclassification, and increasingly difficult to modify.

The calculations themselves may remain technically correct. But the structure that connects them becomes fragile, dependent not on embedded rules, but on careful and continuous manual maintenance.

Section 3

Hierarchy and Aggregation Logic in Traditional Models

A well-structured financial model depends on two foundational elements:

- A clearly defined hierarchy

- Explicit aggregation logic

Hierarchy defines where financial elements reside within the organization. Aggregation logic defines how values roll up across those levels. The distinction is subtle but critical: hierarchy establishes placement, while aggregation determines calculation flow.

Consider a simple reporting structure. A department may roll into a division, that division into a campus, and that campus into institutional totals. At the same time, funds may overlay an additional reporting layer that cuts across that vertical structure. Each roll-up depends on consistent formulas and references. If even one layer is defined differently in another worksheet, totals can diverge without being immediately obvious.

When hierarchy is manually constructed, structural inconsistencies can emerge. Roll-ups may be defined differently across worksheets. Totals may rely on hard-coded references rather than dynamic ranges. Exceptions may be introduced for specific reports. Structural rules may not be documented in a way that makes them visible to other users. Over time, this creates a model that technically calculates correctly but relies heavily on disciplined maintenance.

As complexity grows, maintaining consistent aggregation logic becomes increasingly demanding. Adding a new department, for example, may require:

- Updating multiple summary sheets

- Adjusting reference ranges

- Verifying that no formulas were missed

Each addition introduces new dependency paths. In technical terms, traditional modeling hierarchy functions as an aggregation network without structural guardrails. It operates correctly only as long as every roll-up and reference is maintained carefully and consistently.

Section 4

Attributes and Multi-Dimensional Reporting

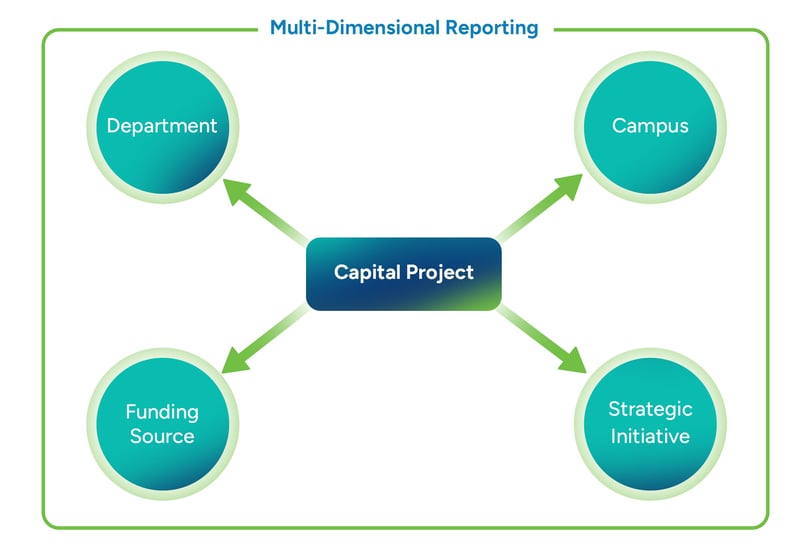

Vertical hierarchy defines where financial elements sit within the organization. But institutions rarely analyze performance from only one vertical perspective. Beyond formal reporting levels, leaders often need to examine financial activity across alternative dimensions that cut across the hierarchy.

For example, a capital project may simultaneously belong to:

- A department responsible for execution

- A campus or service area

- A funding source such as bonds or restricted funds

- A strategic initiative aligned with institutional priorities

Each of these classifications serves a different purpose. Department leaders focus on operational responsibility. Central administration may evaluate funding capacity. Trustees may examine alignment with long-term strategy. These perspectives do not replace the primary hierarchy, they exist alongside it.

In user-maintained models, accommodating these lateral views often requires building parallel reporting structures. Projects may be duplicated across tabs to satisfy different audiences. Separate roll-up sheets may be created for funding sources or strategic initiatives. Summary structures may be rebuilt multiple times to support alternative perspectives. While this approach can deliver flexibility in the short term, it introduces structural risk. As objects appear in multiple locations, placement may become inconsistent, totals may diverge across reports, and competing versions of the same hierarchy may emerge.

What initially appears to be flexibility can gradually become structural fragmentation.

True multidimensional analysis requires both a stable primary hierarchy and a consistent method for grouping financial elements across alternative dimensions. When these mechanisms are not structurally embedded, they must be engineered and maintained manually. As additional dimensions are layered in, the effort required to preserve consistency increases, and the risk of divergence grows.

In governance-driven environments such as Higher Ed and public finance, the ability to view the same financial element through multiple lenses without duplicating or reclassifying it is not simply a convenience — it is a structural necessity.

Section 5

Structural Risks of User-Defined Hierarchy

When organizational structure is manually defined and maintained, consistency depends heavily on individual discipline. Over time, even carefully constructed models can begin to drift. Roll-ups that were originally aligned may vary slightly between reports. Classification rules may be applied inconsistently. Assumptions about placement may live in practice rather than in documented logic. What begins as a clear hierarchy can gradually become a collection of loosely coordinated aggregation paths.

As structure grows more complex, ownership often becomes concentrated. One individual may understand how departments roll into divisions, how funds overlay reporting layers, or how exceptions were handled in past reorganizations. If that knowledge is not embedded into the model itself, it resides in memory. This creates vulnerability during staff transitions or institutional change.

Error exposure also increases in user-defined hierarchies. Financial elements may be placed incorrectly within summary structures, particularly when new departments, programs, or funds are introduced. Small misclassifications can ripple upward, affecting totals presented to leadership or oversight bodies. The calculations may be technically correct, but if placement is inconsistent, interpretation becomes unreliable.

Maintaining structure also requires ongoing time investment. Hierarchies must be manually updated, roll-ups verified, and reference paths checked each time organizational changes occur. Over time, structural updates become disruptive. Once hierarchy is embedded deeply in formulas and references, modifying it can require widespread revision rather than targeted adjustment. Flexibility decreases precisely when institutions need adaptability most.

These risks are especially significant in governance-driven environments. In Higher Education, reporting structures often span departments, schools, campuses, and institution-wide summaries, with additional complexity introduced by restricted versus unrestricted funds and accreditation oversight. In public utilities, classifications such as operating versus non-operating, capital versus rate-based reporting, and debt covenant compliance views introduce multiple structural layers that must remain aligned. In municipal governments, fund accounting, department-level reporting, program classifications, and council-level summaries create similar structural demands.

Learning Objectives Recap

By the end of this module, learners should be able to:

Explain how traditional models rely on user-defined hierarchy.

Describe the role of aggregation logic in roll-ups.

Identify risks introduced by fragmented structural evolution.