Section 1

What is a Business Object?

A business object is a structured representation of something real within an institution. It’s an element that exists operationally, follows defined rules, and changes over time as conditions evolve. Rather than thinking in terms of isolated line items or totals, business objects reflect how financial activity actually occurs in practice.

What distinguishes a business object from a simple row or subtotal is that it bundles related assumptions, drivers, and calculations into a coherent unit. An employee group is not merely a compensation line. It reflects headcount, wage growth, benefit rates, and turnover patterns working together over time. A ratepayer class reflects usage volumes, rate structures, and growth behavior. By organizing financial logic around these structured elements, models more closely mirror how decisions and operational realities influence results.

Business Objects in Traditional Modeling

In traditional modeling environments, there is no built-in concept of a “business object.” Instead, experienced modelers often apply structure intentionally. They group related assumptions and calculations together to represent something real within the institution.

For example:

- A student cohort may include enrollment, retention, price, and discount assumptions grouped in one section.

- An employee group may combine headcount, wage growth, benefits, and pension logic.

- A ratepayer class may bundle usage volumes, rate tiers, and growth trends.

When done well, this approach improves clarity and consistency. However, in manually structured models, this structure is not enforced. It is a modeling choice. Two analysts can build similar models using very different structures. Over time, even well-organized models can drift as updates accumulate, additional dimensions are layered in, or new users make changes.

In traditional modeling, organizing logic into object-like groupings is considered a best practice, but it depends entirely on user-discipline.

Section 2

Why Structure Becomes Difficult to Maintain

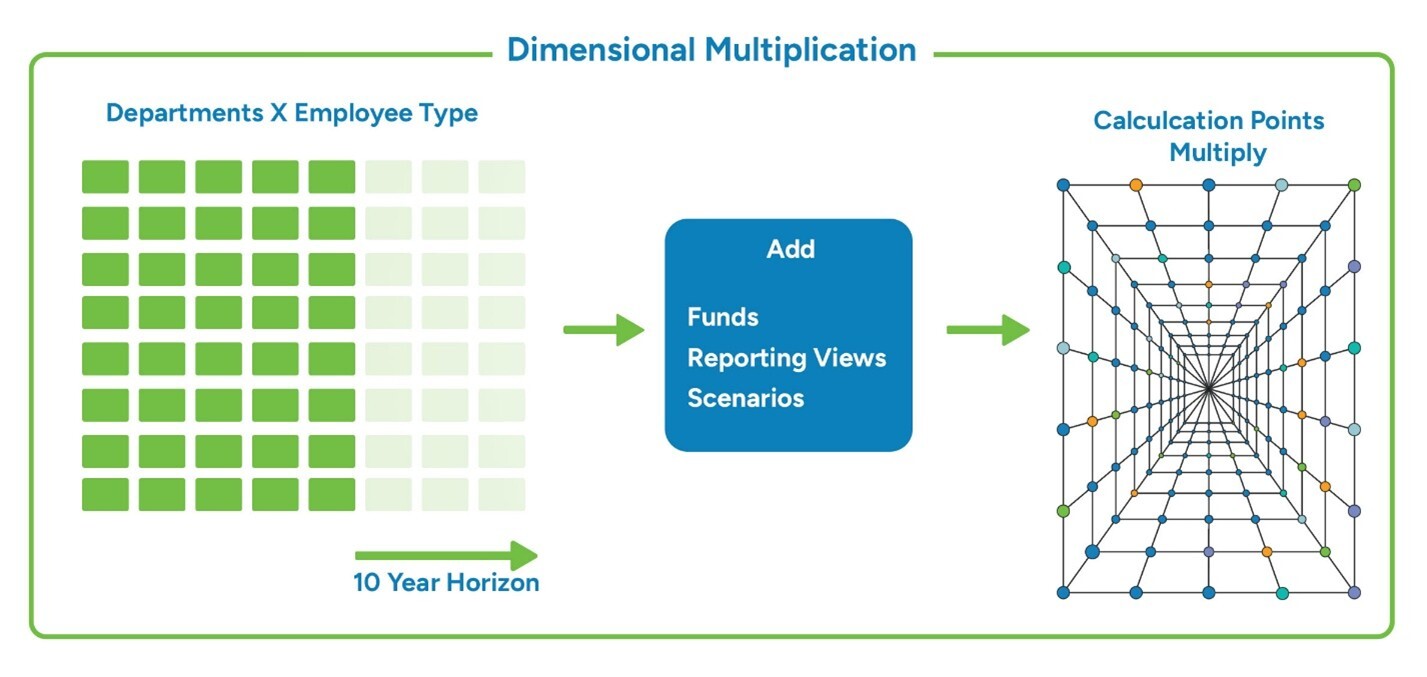

As models expand, maintaining consistency becomes exponentially more demanding. Consider a workforce model that includes eight departments, five employee types, and a ten-year horizon. At a minimum, that creates forty distinct workforce components repeated across time. If each of those components carries five or six assumptions and several calculation formulas, the model quickly grows to hundreds of parameters and well over a thousand time-based calculations.

Complexity rarely stops there. Add multiple funds, alternative reporting views, or scenario comparisons, and the number of calculation points multiplies again. What began as a structured design gradually becomes a dense network of interdependent logic blocks, much like the image below.

In user-managed environments, predictable patterns emerge. Calculation blocks are copied and modified rather than extended from a shared structure. Assumptions become embedded directly within formulas. Similar components evolve differently as incremental updates are applied locally rather than centrally. Over time, structural alignment depends less on architecture and more on vigilance.

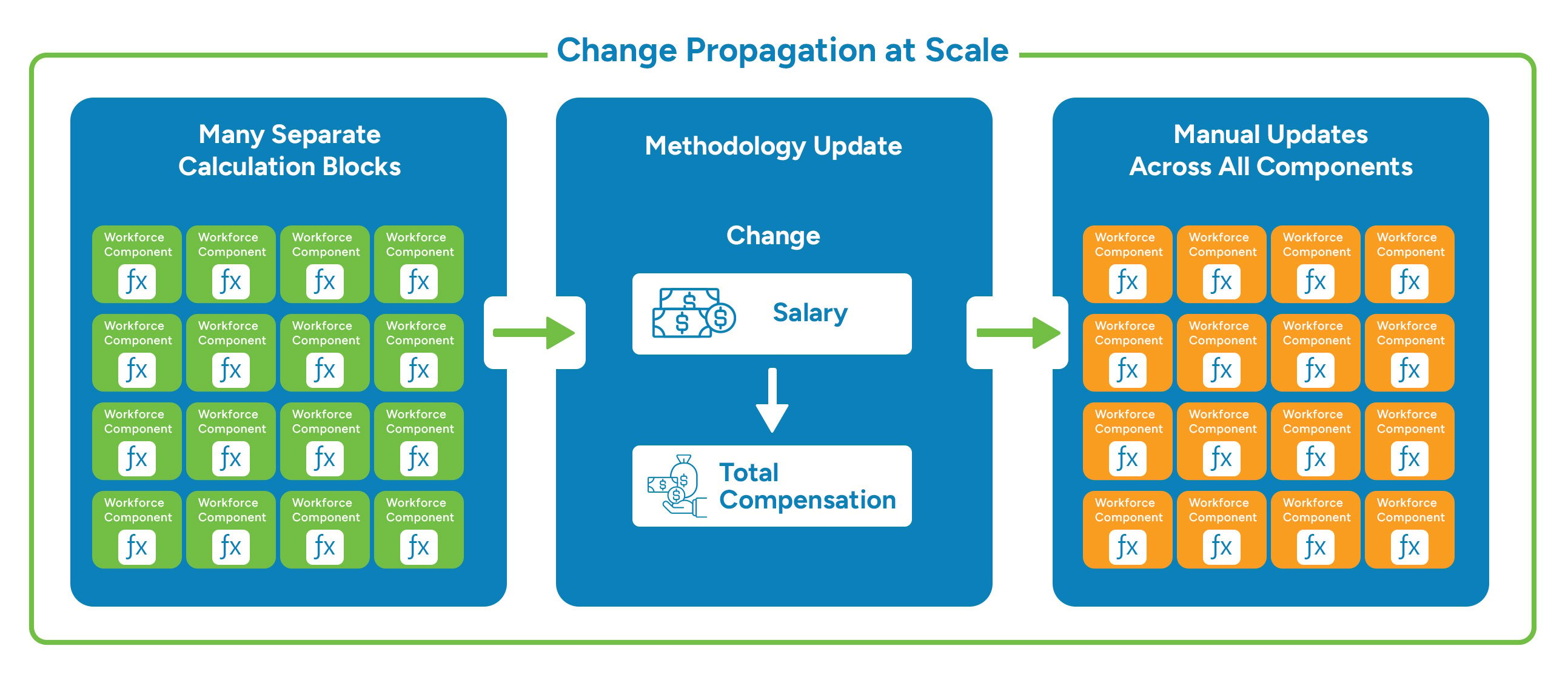

Now consider a methodological change. If the model shifts from projecting salary expense to modeling total compensation, including benefits and pension contributions, every relevant workforce component must be updated. Each formula block must be located, modified, and reviewed individually. Even with careful attention, inconsistencies can arise, not because of poor modeling, but because the structure itself relies on manual enforcement.

The challenge is not analytical skill. It is architectural. When structure is maintained through discipline rather than design, best practice must be continuously remembered and reapplied. As dimensional complexity grows, so does the burden of maintaining consistency.

Section 3

Risks of User-Managed Structure

When model structure depends on individual discipline rather than embedded design, consistency becomes fragile. Similar components that begin aligned may gradually diverge as updates are applied unevenly. Assumptions may be revised in one area but overlooked in another. Reporting dimensions often require duplicating calculation logic rather than extending it, increasing the number of structural touchpoints that must be maintained. Over time, maintenance effort rises steadily, and reconciliation becomes a routine part of the modeling process. As that effort increases, confidence in outputs can erode, not because the math is incorrect, but because the structure supporting it becomes difficult to validate.

These risks compound as models scale. What begins as manageable complexity can evolve into a system of loosely coordinated calculation blocks, where understanding the model requires institutional memory rather than structural clarity. Updates feel disruptive.

Methodology changes require extensive review. Even small inconsistencies can ripple across reporting views and create uncertainty during high-stakes discussions.

This dynamic is especially relevant in public-sector and Higher Ed environments, where models must withstand both operational scrutiny and external oversight. For example:

- Enrollment and tuition projections require scenario testing across multiple cohorts and funding sources.

- Ratepayer structures influence public-facing rate cases and regulatory filings.

- Workforce and pension assumptions shape long-term sustainability analysis.

- Financial projections must endure audit review, accreditation processes, and governing board evaluation.

In these contexts, structural fragility is not merely an inconvenience—it becomes a governance risk. When financial logic is difficult to trace or reconcile, decision-making slows, explanations become defensive, and trust in the model’s outputs can weaken. Maintaining structural integrity, therefore, is essential not just for analytical precision, but for reliable and transparent decision support over time.

Section 4

Structured Business Objects and Model Integrity

When structure is embedded rather than manually enforced, the integrity of a financial model changes fundamentally. A structured business object framework can create a clearer and more consistent foundation, where core elements are defined once and applied uniformly throughout the model. The same logic governs behavior across departments, funds, programs, and time periods. This consistency reduces ambiguity and helps ensure that similar activities are modeled in similar ways, even as the organization grows or reporting needs evolve.

Just as importantly, structured objects create closer alignment between financial logic and organizational reality. Because each object represents something that actually exists, such as a workforce group, a customer class, or a capital asset, the model reflects how the institution operates rather than how calculations happen to be arranged. This alignment makes results easier to explain to stakeholders, who can trace outcomes back to familiar operational components instead of abstract formulas.

Finally, shared object logic builds confidence in how change flows through the model. When assumptions or methodologies are updated, those changes propagate predictably and consistently wherever the object is used. Analysts can be confident that updates affect the entire model as intended, without requiring manual reconciliation or exhaustive cross-checking. As a result, models built on structured business objects are easier to manage over time, easier to communicate, and far more resilient as institutional priorities and conditions evolve. These structural distinctions form the foundation of how financial models scale and remain reliable over time.

Learning Objectives Recap

By the end of this module, learners should be able to:

Define what a business object represents within a financial model.

Describe how traditional models rely on user-managed structure.

Explain why dimensional expansion increases maintenance complexity.